#32 in Books > Business & Money > Personal Finance > Budgeting & Money Management

#197 in Books > Self-Help > Success

More about the author

Vicki Robin is a prolific social innovator, writer and speaker. She is coauthor with Joe Dominguez of the international best-seller, Your Money or Your Life: Transforming Your Relationship With Money and Achieving Financial Independence (Viking Penguin, 1992, 1998, 2008). It was an instant NY Times best seller in 1992 and steadily appeared on the Business Week Best Seller list from 1992-1997. It is available now in eleven languages.

Her new book, Blessing the Hands that Feed Us; what eating closer to home can teach us about food, community and our place on earth (Viking/Penguin 2014) tells how her experiment in 10-mile eating not only changed how she ate, but also renewed her hope and rooted her in her community. She calls this “relational eating.” She went on to investigate how we might restore the vitality of our regional food systems so everyone could have the benefit of relational eating – healthy food, healthy communities. She calls this building “complementary food systems,” not to replace but to work along side of the global industrial systems we now depend on for almost 100% of our food. Her book offers many practical tools for transformation, from changing our attitudes, to changing our habits to changing our food sources to getting active in social and political change.

Called by the New York Times as the “prophet of consumption downsizers,” Vicki has lectured widely and appeared on hundreds of radio and television shows, including "The Oprah Winfrey Show," "Good Morning America" and National Public Radio's "Weekend Edition" and "Morning Edition"; she has also been featured in well over 100 magazines including People Magazine, AARP, The Wall Street Journal, Woman's Day, Newsweek, Utne Magazine and the New York Times.

Vicki has helped launch many sustainability initiatives including: The New Road Map Foundation, The Simplicity Forum, The Turning Tide Coalition, Sustainable Seattle, The Center for a New American Dream, Transition Whidbey and more. In the 1990’s she served on the President's Council on Sustainable Development's Task Force on Population and Consumption.

In addition to her sustainable consumption work, Vicki has been a leader in the field of dialogue. She co-created the Conversation Cafés method and initiative, promoting it first in Seattle and then throughout the world. Conversation Cafés are hosted conversations among diverse people in public places on subjects that matter. Vicki has spoken at workshops, conferences and to the media (Readers Digest, National Public Radio, Utne Magazine, The New York Times, The Seattle Times and many local media) about the Conversation Café method and its possibilities for revitalizing our public life.

For fun, Vicki is a comedy improv actress, appearing frequently with her troupe, Comedy Island.

Born in Oklahoma in 1945, Vicki grew up on Long Island and graduated cum laude from Brown University in 1967. She received awards from Co-op America and Sustainable Northwest for her pioneering work on sustainable living. Vicki’s one of 61 visionaries featured in Utne Magazine’s book, Visionaries: People and Ideas to Change Your Life. A&E Entertainment’s show “Biography” honored Vicki as one of ten exceptional Seattle citizens. She currently lives on Whidbey Island in Puget Sound.

Editorial Reviews

Review

Recommended by Millennial Money, The Simple Dollar, Mr. Money Moustache, and other top financial bloggers

"The best book on money period." -Grant, Millenial Money

"[Your Money or Your Life] changed my life...I started believing that my life controlled my money. I began to see my life without the weight of debt and the need to chase a paycheck because I actually understood the path to get there." -Trent Hamm, The Simple Dollar

"Your Money or Your Life is a wise book...I am thankful to Joe Dominguez and Vicki Robin for getting so much of this started, as are countless thousands of other people who are now more free than they could have otherwise been." -Mr. Money Moustache

"This is a wonderful book. It can really change your life." -Oprah

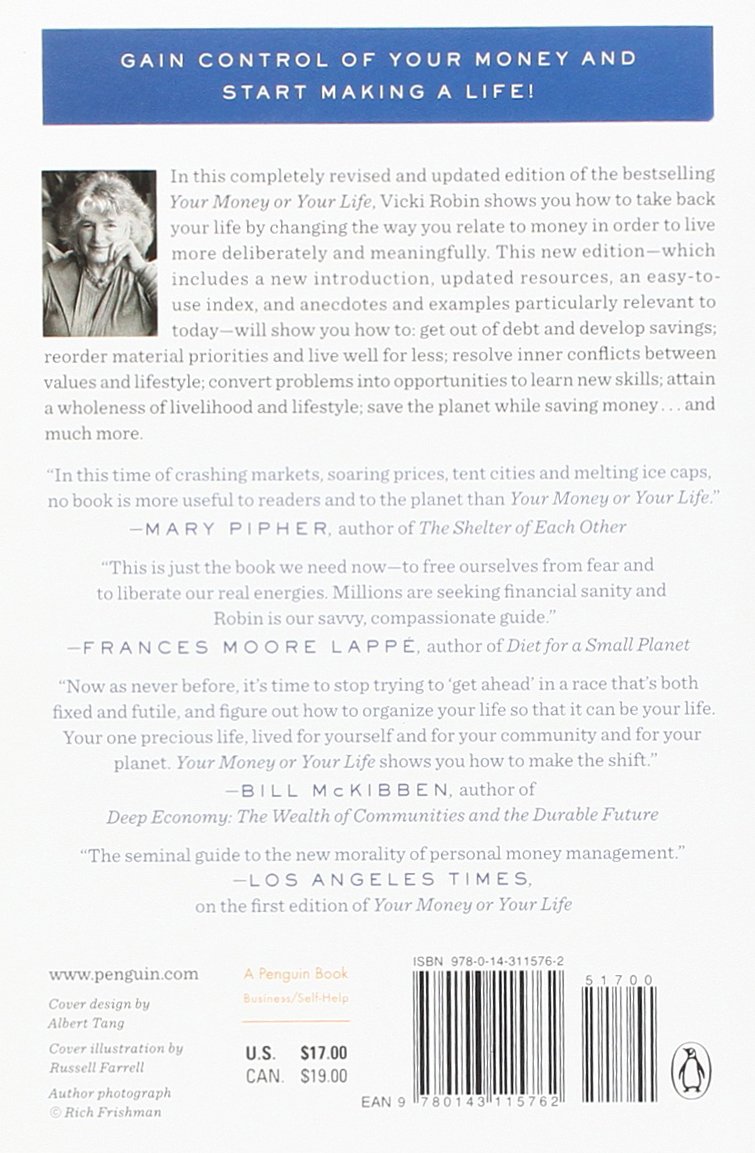

"The seminal guide to the new morality of personal money management." -Los Angeles Times

"Now as never before, it's time to stop trying to 'get ahead' in a race that both fixed and futile, and figure out how to organize your life so that it can be your life. Your one precious life, lived for yourself and for your community and for your planet. Your Money or Your Life shows you how to make the shift." -Bill McKibben

About the Author

Vicki Robin is a renowned innovator, writer, and speaker. In addition to coauthoring the bestselling Your Money or Your Life, Robin has been at the forefront of the sustainable living movement. She has received awards from Co-Op America and Sustainable Northwest and was profiled in Utne Magazine’s book Visionaries: People and Ideas to Change Your Life. She is also the author of Blessing the Hands That Feed Us: What Eating Closer to Home Can Teach Us About Food, Community and Our Place on Earth. She lives on Whidbey Island in Washington.

Joe Dominguez (1938-1997) was a successful financial analyst on Wall Street before retiring at the age of thirty-one by following the nine-step program he formulated for himself. He taught this formula for many years, and preserved it for future generations in Your Money or Your Life. From 1969 on, he was a full-time volunteer and donated all proceeds from his teaching to transformational projects.

Customer Reviews

4.0 star

Useful Information

ByRandom Amazon Shopperon December 4, 2016|Verified Purchase

I found this book worthwhile, but not what I would call 'the perfect solution". I am over 70 and have spent my life living frugally, continually saving and investing for the future and retirement. I have been quite successful at growing net worth, while living comfortably. I truly believe a key component is learning who you are and understanding how you are best suited to reach your goals. I personally think this book is too caught up in looking at every penny. I think each penny is important, but have focused on being sure there is constant savings. I don't expect my approach to work for everyone, but I want to emphasize that there can be many paths to reach the same goals. I suggest reading a wide variety of approaches that focus on saving and investing for the long haul. I have made small changes along the way when trying new things. In the end I have found that success came with simplicity. Look for the big picture in the book and any other. Growing wealth is like growing a big tree, strong trees grow big over a long time.

2.0 star

last two chapters most useful and can be read in a bookstore

ByAmazon Customeron January 9, 2017|Verified Purchase

Basic principles of this book are decent, however, the principles are not gold and it could be summed up well in 50 pages or less...not the redundant, ranting 300 page book it is.

First 80 pages of the book are worthless and torture mostly focusing on the consumerism/doomed/horrible smog-infested society we live in, last two chapters most useful and can be read in a bookstore.

I did not like many examples given; it seemed to focus on divorce excessively with ~ 80% of case report examples of "FI-ers" being divorced which I found rather odd and unnecessary to mention.

Take home points of this book: Spend less than you earn, save, document every penny you spend, become a minimalist and only purchase things you need, the less you need the more fulfilled you will be, the less you will work, etc.

Things to consider:

1) The "FIer" lifestyle is not for everyone- I equate an "FIer" to the tiny home movement in principle.

2) Book recommends that bonds should be the mainstay and the only thing in your portfolio. I strongly would discourage this. "Safe" bonds which I pretty much consider anything that that is not a junk bond or preferred stock bond, are not hitting the high yields that Joe Dominguez saw in his day and on many years aren't comparing to rises in inflation. While you can never predict the stock market, when looking at time tables- it always goes up. Traditionally, stock markets rise while bond yields go down some and visa versa. The best way for security and safety is proper allocation to each of these modalities: bonds (treasury bonds are great as mentioned in the book because you aren't charged state taxes, however, what the book fails to remind you of is that federal taxes are still fair game) and diversified stock portfolio most safely done by investing in mutual index funds with low fees (e.g. Vanguard). The older you are, for safety, the more bonds you should have in case the stock market plummets during your retirement years. For conservatives a 60% mutual funds and 40% bonds is recommended. For a retirement person, 20% stocks and 80% bonds should be considered. When you have all your eggs in one basket, you lose that safety net.

3) Other things I disagree with in this book- everyone should have health insurance, you should not forgo this to "save" money; sure buy the less comprehensive plan if you are healthy and pay less and have a higher deductible but you are gambling when you forgo it all together.

4) They also suggest in this book "rolling-over" your 401k and 403b accounts to bonds; however, these are pre-taxed dollars and you will likely get slammed- most retirement plans now give options to the "risk" or rather stock/bond ratio you desire. I would more likely suggest rolling money to Roth IRAs (post-tax and therefore tax free with capital gains) or just leave your nest egg to compound growth where they are at.

Now I am ranting. Cheers.

4.0 star

This book is so full of great information readers may need to hire a life coach for support to get through the demanding steps

BySteve Schulloon June 8, 2017|Verified Purchase

I have read many books on personal finance. The majority were about the quantitive aspect: the data, graphs, statistics, market history, types of stocks and bonds, and the skills needed to construct low-cost diversified portfolios. This book finishes the job by discussing the lesser status qualitative aspect: your thinking and your emotions surrounding money. Both aspects make valid contributions for the eventual, sometimes elusive goal of financial independence, and to be happy at your job and giving back to the greater good.

I had never heard of this book until I listened to a podcast interview by Mad Fientist. After reading the book, I understood every sentence because at age 69 I was lucky enough to have lived through much of the good information found in the book. I recommend it because the authors elaborate and explain in great detail not only how to achieve financial independence with quantitative strategies (Step 9) but find your metaphysical space.

My definition of metaphysical space is that most people need more than just the quantitative thinking about getting enough money, or getting rich, which most people think it will never happen anyway. Many DIYers complain about the investing public not interested, perhaps they are not interested because they find all of the great books on personal finance dry and impersonal. Don't get me wrong I love those books but I also love what the authors say in this book. We need both aspects so that more people know why they are saving and investing to keep slowing building wealth over a working lifetime. Without answering the why, most people give up, and find investing too difficult.

Steps 1-8 provide the "consciousness raising" and motivation for staying the course throughout your life. Remember the title "Your Money OR Your Life." The authors skillfully put the two opposing topics (money or life) together. Based on my experience I would have never stayed the course without the 10,000 foot perspective of the bigger issue of financial independence that is layed out in Steps 1-8.

I gave the book four stars because of the confusion of Steps 8 and 9 (I elaborate at the end of this review, and a ridiculous and irresponsible comment that should have been deleted). The authors cover all that needs to be included, which is a disadvantage because there is so much useful information that readers would need face to face support to complete each step. Readers should not expect themselves to do all the steps quickly, but take a few years to get your thinking right and your skills sharpened.

The authors begin where it needs to be started: In Your Head! I love the author’s big picture explanations, and their ultimate goal, quoting: “It is the authors’ fervent hope that this book will increase your freedom to contribute to the world.”

YEAH! I think we all want the freedom to give back our values and our passions to the greater good. The authors took great pains to lead their participants to find that connection between your heart, passions and values in everything you do, especially your time working for money. They cited a famous book on that subject, which I read in my younger years, Bolles’ “What color is your parachute.”

What a challenge! Becoming a positive and contributing member of society by changing our Western Culture’s (especially American culture’s), relationship with money is a HUGE undertaking.

Oh my god! Changing people’s relationship with money in our current borrow and spend culture, IMO, is as difficult as paying off the national debt or obliterating the electoral college—it ain’t going to happen anytime soon.

Yet, I applaud the authors' extraordinary courage for working on improving this relationship. Even though the profound effect of our consumer culture is overwhelming, you don’t have to participate. According to the authors, their participants have already benefited and found authentic happiness. One thing that has been investigated thoroughly is that spending alone is not going to make anybody happy permanently.

We are the richest country in the entire history of the planet, and many Americans are unhappy. The authors cite the National Opinion Research Center that 35% Americans describe themselves as “very happy” in 1957 to 30% in 2002.

What happened?

The authors explain our current dilemma. The reasons are complex, but nothing new:

1. rat race (“more is good” thinking there is no end to using earth resources ever)

2. materialism (The creation of consumers), "We buy things we don't need with money we don't have to impress people we don't like."

3. nonstop “exaggerated” advertising

4. keeping up with the Jones

5. not knowing how and why many Americans are living from paycheck to paycheck with disastrous long-term consequences—stress, divorce, bankruptcy and becoming a burden on medications and society.

The above can be significantly reduced and eliminated permanently, and this book shows how to achieve that excellent goal.

The authors’ recommendations are also nothing new. Many of the world’s oldest and established spiritual institutions show how to empower yourself by reestablishing your thinking to what is important. How do we permanently ignore most if not all the expensive, negative and noisy world “out there?”

The authors were brilliant on explaining in detail what you can do now, each day, NO MATTER what is happening “out there.” It’s about empowering yourself because nobody else is going to change—you have to change.

Step 1: Find out how much you have already earned. Most working people go through $2-4 million in their professional life ($75,000 average over 40 years = $3,000,000) and yet most people have not saved one penny. As you become aware of the huge amounts of money that comes and goes through your wallet or purse, without thinking, you will find the motivation to plug some spending leaks (Hint: purchase a two-year-old pre-owned car and keep it for ten or more years).

Step 2: This is about calculating what you earn an hour. It is a complicated step. They offer an example of a person making $17.00 per hour but end up only taking home $6.00 per hour because of working expenses.

I understand the costs of commuting and work-related clothing, but they also factored in:

1. meals (my comment: must eat no matter what!),

2. decompression (my comment: must rest no matter what!),

3. escape vacation (my comment: what? It’s that what vacations are for?)

4. and job-related illness (my comment: never ending question of how did I get a cold or flu. Why blame the job? Besides, those employees who have sick hours should not be deducted and those unfortunates who don’t have sick time are not paid because they are not working).

Thus, I don’t agree with their above calculations that leave only $6.00 an hour. Most of the above expenses are not work related to the degree that the authors intended. They didn’t have to exaggerate to make their valid point, but they use the $6.00 per hour example for the rest of the book.

They insist on paying attention to EVERY CENT. I agree that some people may need to pay attention carefully. But it’s not encouraging, and another reason I gave this book four stars. Step 2 is a difficult sell because it is tedious and time-consuming, and the reason why most people probably give up.

Step 3: I applaud the authors' participants who followed up with this complicated step. If you have serious spending problems and can do 20%-30% of this step, and stick with it, you will be in great shape. The conversion of dollars into their “hours of life energy” puts this step over the top IMO. It’s a great idea, but too much work and time to do this on your own without additional support. People want things simple to implement, but this step is time-consuming and discouraging without their steady support network. For the casual reader, it’s out of reach without face to face support, and commitment from participants.

Step 4: The chapter is more of a philosophical than a practical guide. Establishing what makes you happy in what you do has been written in hundreds of career-type books, and practiced by many current life coaches.

The authors published their book just before one of my favorite authors, Jack Bogle, published his book, called “Enough.” He is the founder of Vanguard. This chapter is about discovering when you have “enough.”

Step 5, “Seeing Progress”: The wall chart is a great innovative idea. People need to see progress to their personal “Crossover Point.” Their wall chart is one of their best ideas and easiest to implement.

Step 6: The authors are now getting somewhere close to my heart, and scored another valid and significant contribution to the entire discipline of personal finance. To achieve FI, we have to live frugally, and frugal living is NOT boring! The authors spell this out in the “Pleasures of Frugality.” And just ask the most famous frugal family of all time, Mr. Money Mustache, his wife, and young son from his brilliant blog posts.

Personally, I have naturally lived the frugal and a wonderful life for 69 years. I have traveled the world, lived in nice homes in expensive Southern California on two public school educator’s salary (late hubby was an educator too), had a terrific professional career (but low pay), and a grew a comfortable, secure retirement. Below is a partial list of what the authors recommend getting to this peaceful and happy place:

1. work hard on discovering what motivates you and why

2. live below my means (magical experiences happen because material distractions “distract” from your mindfulness regarding having “enough” and valuing “inner” experiences over “external” material things)

3. discover how and why to stop the never-ending rat race, and stop impressing others

4. discover gratefulness on what you have now, and all the great information the authors said about empowerment and finding your values.

The point of this step as the authors wrote: “Learn to choose the quality of life over a standard of living.” If you can get to this stage, you will have changed your relationship to money, along with your wellbeing and heighten your ability to assist others. The authors did not mention, that I recall, about learning from all mistakes, especially the most painful, a valuable commodity that only you own.

Step 7: What a great step, Valuing Your Life Energy—Work and Income.” The topics about valuing what you do for pay are truly exceptional and worth the price of the book alone. This step is so deep and profound it may require the help of a life coach to appreciate and experience.

My one caution is about one of their points, “How to Get a High-Paying, High-Integrity Job.” Nothing wrong with high pay but when you inform people, they might begin to expect higher income because your values and work are one in the same is a risk. For me, this expectation takes away from the primary purpose of this step. It sounds wonderful, but there are two realities to keep in perspective especially with regards to work for money: fantasies and realities. My goodness if your fantasy and reality are a match, it is great. But not all of us can achieve this fairy-tale type match, anywhere near 100%. I applaud those lucky folks who are indeed successful, inside and outside such as the authors themselves and their many participants.

After reading Bolles book several times myself in my younger years, I never saw an increase in my income. But I found a job that paid me contentment and satisfaction, but not in hardcore wages. That’s the point! In fact, I entered a low-paying public teaching profession because it matched my values, and I needed a job.

All those great value connections you discover may go out the window if you expect a high-status, high-income job.

And I was further confused by on page 197, “…the higher the pay, the more time you can have for other things that matter to you.” Sorry, but this sounds more like a sales pitch.

Step 8: Making it to the “Crossover Point”. This point is monumental in everybody’s life. I didn’t get to this point when my investments and pension took the place of my wages until I was 61 years old. It feels so good to be able to replace paid income with income from your investments.

However, in Step 8 the authors recommend saving your money in a fixed account during your working lives. Then when you retire, you can create a stock and bond balanced fund. This advice is inaccurate at best and dangerously out-of-date at worse. My message to young people: DO NOT WAIT! Invest in a low-cost and balanced equity and bond portfolio in your 20s and 30s!

Both Steps 8 and 9 needs to be combined and updated.

However, in Step 9, their advice about index funds, hiring a professional and watching costs are spot on. The author’s recommendations made great sense on the following topics:

1. watching investment costs

2. recommending the National Association of Personal Financial Advisers for fee-only fiduciary advisers

3. take on more responsibility by making your investment choices and watching your adviser’s costs

4. better yet, discover how to manage your investments without an adviser (highly recommended by this reviewer)

5. discover the passive strategy with low-cost index funds

6. discover lifestyle funds

Two examples of outdated and dangerous advice:

1. They wrote (but later corrected, I think, in this step 9) that stocks and real estate are “speculations.” Nothing is further from the truth. Broadly diversified index stock and bond funds are not speculative (My comment: Investing in Ostridge farms, your brother-in-law’s business startup, or investing any of your assets in one company stock are as speculative as gambling in Las Vegas. They fail proper asset allocation and diversification).

2. The following comment from a participant was atrocious and dangerous, and should have been deleted. Page 276: “…we were willing to live without health insurance. One of the by-products of working the steps was that we had because much more fearless about life, so the prospect of going without health insurance did not daunt us.”

Yikes! This participant’s comment reflects a grave misunderstanding about risks. The authors were discussing equity risk in a balanced portfolio, not risking your assets by going without medical insurance. Think of the small businesses which lost everything through personal bankruptcy because the owner got sick. No matter what, always try to purchase affordable health insurance.

Sum,

Steps 1-7, 9 makes it one of the best books on the general subject of personal finance. Just some minor concerns about Step 7 which needs to delete the misleading comment that incomes will increase if you match your life values with your work for money. Step 8 is out-of-date with saving in bonds for your working years. Even though the authors explain further in Step 9, it makes the ending a bit confusing.

2.0 star

laborious and tedious advice. Only made it through about 40 pages ...

ByAmazon Customeron December 29, 2016|Verified Purchase

Meh. . . laborious and tedious advice. Only made it through about 40 pages until I was bored out of my skull.

5.0 star

and pass it on to those you love. Put its message into practice

ByLauraon January 17, 2016|Verified Purchase

This is probably the most influential money management book I have ever read, and I have read dozens. Other reviewers have summarized the book's content/message well, so I won't be repetitive. If you are even slightly considering this purchase - BUY THIS BOOK! Read it, re-read it, and pass it on to those you love. Put its message into practice, and you will enjoy a return on this particular investment a thousandfold, if not many times more.